The Essential Guide to Syndicates

The following is from a piece I posted on my blog in early 2021. Reposting it on substack for additional visibility!

First off, hi! I’m Paige, author of a children’s book for adults on venture capital, a Developer Success Engineer at WorkOS, an early stage syndicate lead, and now working on my first fund investing in product-led growth companies & focusing on GenZ & underrepresented founders.

I’m passionate about democratizing access to information and capital in the venture space for founders, technologists, creators, and aspiring investors defining the future of work. My goal for the next ten years is to help 1,000 people make their first angel checks, 500 people organize their first syndicate, and seed 100 emerging managers. ESPECIALLY underrepresented folks.

Follow me on twitter @paigefinnn for more accessible venture capital content. If you organize a syndicate based on the content I shared below, please DM me & let me know – I’m tracking this goal!

If you prefer video, feel free to watch me talk through this guide here:

The Essential Guide to Syndicates for Aspiring Investors

In this guide, I’ll broadly define what a syndicate is, how to work with syndicates and why you should consider them as part of your fundraising journey as an organizer, an investor, or a founder. Feel free to comment any questions you may have!

Special thanks to Halle, Abena, Pravani, Sean, Arry, Jeremy, Siraj and Dalia for proofreading this!

So, what is a syndicate?

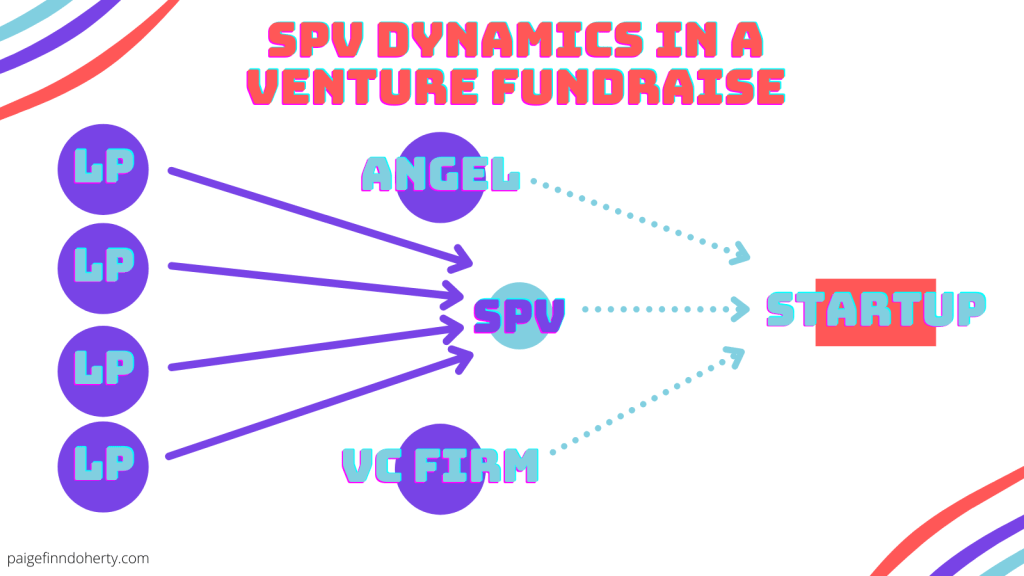

A syndicate is essentially a deal by deal venture capital firm. It’s composed of an organizer (or organizers) who makes investment decisions, and backed by accredited angel investors or high net-worth individuals who contribute capital (referred to as a limited partner or LP). An organizer may have a consistent base of investors they work with across deals, but they may not be the same for each deal because each LP can opt in or opt out on a deal by deal basis. Each deal is either referred to as a syndicate deal or as its legal construction name – an SPV.

So how does a syndicate deal work, really?

First, a syndicate organizer has to secure allocation, or a piece of the round. A syndicate lead secures allocation from their source of deal flow – either inbound interest from the founder or via cold outreach. For example, the source of my first syndicate deal came from a community number that I set up to share updates for my book Seed to Harvest. Some of my friends have gotten allocation through cold outreach via Twitter DMs or email.

To get into a deal as a syndicate lead, you’ll most often punch above your weight in what Harry Hurst, the CEO of Pipe, coined the “Check Size : Helpfulness” ratio. As a syndicate lead, you’ll engage in a due diligence process with founders, going through their pitch, your questions, and possibly reaching out to a few investors in your syndicate to gauge their appetite for the deal. You’ll negotiate allocation after deciding to invest in the company. Syndicate allocations, according to AngelList, on average range from 200k-300k, but I’ve seen a range from 50k – 400k.

From here, each syndicate organizer runs their process differently. I send an update email out to the accredited investors on my syndicate list, which are tagged by area of interest & check size. They’ll usually reply with more questions, or a yes or no. These yes’s (and their associated check sizes) are called commitments. They’re not legally binding but are rather held by someone’s word; I keep track of them in a google sheet.

After receiving commitments, I use a platform called Assure (assure.co) to to handle the fund administration side: create a legal entity, provide SPV fund documents, a bank account, taxes, distributions, technology (Glassboard) and all the other things associated with the Special Purpose Vehicle (SPV) created to invest in this company.

A note on using fund administration software: Using a software platform like Assure decreases the traditional fund administration process by as much as 90%. Assure has multiple one-time pricing options. Their starter package charges a one-time fee of $2,500 and 1.5% of the raise plus any blue sky fees (tax that states charge funds) plus a distribution fee if and when there is a future distribution event, Assure handles most of the fund administration previously handled by lawyers, banks, admins, and tax professionals. AngelList is a great option if you’re looking for a full vertical solution, including an LP marketplace.

After my commitments reach my allocation level, Assure closes the SPV & we wire the money to the company we’re investing in. Depending on the size of the round, this process from securing allocation to “close” has taken me ~3 weeks. Most of this time is spent waiting for granular details, like the bank account set up & the wire confirmations from investors. After this ‘close,’ I sent out an intro email with a blurb introducing all my LPs to each other & also the founders.

For more information about using Assure, feel free to check them out here or DM Landon (@LandonAinge), the Managing Director of Assure Syndicates on Twitter (he’s awesome & has been so helpful in my syndicate journey).

Why is organizing a syndicate a good idea for an aspiring investor?

You are not required to be an accredited investor to be a syndicate lead. Even though you are required to be accredited to invest, you can start your investing career and begin to build a network and track record by leading deals. Assure will work with non-accredited organizers.

Pros

Practice on reaching out to LPs and writing deal memos to get LPs excited

Opportunity to build a track record with top tier VCs co-investing

Build repetition of hyper speed due diligencing

Own your LP relationships

Build & prove out your thesis so that you have immediate access to pools of capital when you find a company that you have really high conviction about

Look at tons of deals & start to understand what’s a good fit for you

Build out process automation for deal flow later on

Founder friendly terms

More formal arrangement than just intros to funding

TIP: trying to focus on angels with similar or tangential interest area cut my reach outs in half vs had I not been specific. The more closely a company aligns with their thesis, the easier it is to reach conviction.

One-off Special Purpose Vehicles, or SPVs (mini-funds compiled to invest in a single company) via Assure – great if you’re looking for high touch support & have an existing network of investors you like to work with.

Subscriptions via AngelList – great if you’re looking for completely self-serve & verticalization of tool plus additional investors than your existing network

Allocations is an additional option for fund administration

“The difference between raising money for an SPV vs. for a fund, is that in an SPV the investor is underwriting the asset (the thing you are about to invest in), whereas in a fund, they are underwriting YOU”

Cons

Lots of work – you’re basically doing all the leg work for the founder for that section of the round with carry-only compensation

The Essential Guide to Syndicates for Investors

So why would you back a syndicate as an investor?

Trend in VC: lots of capital -> saturation -> more competition for deals. It’s a founder’s market, so as a syndicate backer, you’ll have access to competitive deals you wouldn’t have seen otherwise

Maybe you’re starting out & want to write $1k-$5k checks, which most founders with whom you don’t have a pre-established relationship won’t accept directly. You can get into competitive deals through a syndicate lead with a smaller minimum check size.

Another common refrain: I have money, I don’t have the deal flow.

Be involved in the ecosystem & supporting the next generation of emerging managers and founders who bring a diverse perspective to startup funding, which has been shown to generate higher returns

social capital article

Only should be part of your income relegated to angel investing – risky investment but with higher upside

Often no management fee vs working with a fund (only carry)

Ability to opt into deals that you’re excited about and pass on those you’re not

Coinvesting details for funds: https://oper8r.substack.com/p/benchmarks-demystifying-vc-co-investing

Investors need to be accredited. If an accredited investor is interested in investing into a syndicate, they need to complete two tasks: sign the syndicate SPV fund documents and wire funds. Although the list of tasks to invest is short there is plenty of work around making the decision on if you are interested in investing. Here is a quick list of things you should consider.

Minimum investment amount. Each syndicate organizer will set a minimum investment amount. A common amount is $5,000 but some organizers are larger and smaller.

Risk. Every investment has risk and investing into startup companies has a large amount of risk and each investor should be comfortable with and able to lose their invested amount.

Industry and specialty. Many syndicate investors are more interested in deals that focus on an industry, sector or specialty that the investor has interest or expertise.

Time horizon. Startups take time to grow and some startup investments, that don’t fail, can take a decade or longer to reach an exit.

Gather information. To assist in making your decision to invest, it is recommended that you review the materials and attend meetings that are provided to you.

Prepare to move quickly. Not allows but the allocation in the best deals can go quickly so delaying can be a detriment.

The Essential Guide to Syndicates for Founders

Why would you want to work with a syndicate as a founder?

Leverage is really important in a fundraise, so as a founder it can be helpful to enlist a syndicate lead to abstract some of the relationship management while you focus on large check sizes. There’s generally two ways a syndicate is involved:

A Syndicate Lead: Someone else raising a chunk of your round for you: ability to pinpoint specific investor personas since the investors on every SPV are different

What I call a Syndicate as a Service: handling smaller check sizes for you(under 50k) from inbound interest you’ve generated (keeps your cap table clean while still be able to accept smaller angels)

Beyond this, syndicate leads can extend your existing investor network & add their social capital to your round. Many of them can also bring specific operator angels to augment.

A great question I received from one of my syndicate LPs Sean was: As a founder what are some of the key differences (see pros and cons) of an angel investor, a venture capital firm or a syndicate when thinking about funding? Does that change in later rounds?

Angel investors & syndicates are great ways to build momentum when you’re raising & looking for a lead investor for your round. Angel investors can commit the fastest of all groups, since they aren’t managing Other People’s Money (OPM).

Some FAQs:

What’s the best way to set one up? I use Assure.co. @landonainge can help.

If you create a syndicate, what are your obligations after the investment is made? Your obligation is all of the post close activities that the syndicate SPV needs to complete, like tax returns and corporate actions. You will need to make future investment decisions when the syndicate SPV is asked to vote, as an investor on the company cap table. You also have an obligation to your investors to be available and you need to assist with any future distributions. Groups like Assure will prepare the syndicate taxes and assist with all your corporate actions and distributions.

What’s the difference between Syndicates and SPVs? There isn’t anything different between a Syndicate and an SPV, they are exactly the same thing.

How many LPs can you have in a Syndicate? You can have 99 accredited LPs (investors) in a Syndicate. If you are investing in a startup company and your Syndicate raises less than $10M then you can have up to 249 accredited LPs (investors). If your LPs (Investors) are qualified purchasers then you can have up to 1999 investors in your syndicate but if you want to raise capital from more than 99 or 249 (depending on your asset and fund size) every investor must be a qualified purchaser.

What if I want to set up the SPV outside the USA – in the UK or India? [Answer from Siraj] I did some research on this and found that AngelList is a good option for these two countries. They are more expensive ($8000) than Assure and so you have to have a min size of fund raise ($4-500K) to get the economics right.

The legal and taxation challenges in these two countries require an SPV entity that this set up in these countries and that can offer the tax incentives that investors will ask you to provide :

UK incentives – From AngelList website

UK syndicates use a different legal structure to allow UK investors to benefit from EIS and SEIS tax breaks. Backers co-invest into the startup alongside the Lead. We use a nominee, Capita IRG Trustees Limited, to hold shares in the startup on behalf of the Backers.

India Taxes – From AngelList Website:

The return from the carry will be realised only upon a successful liquidation event (e.g. secondary, sale, public offering) and will be shared as per the distribution guidelines mentioned in the investment documents. Typically, 15% carry will be paid out to the Lead Investor and 5% carry will be paid out to AngelList India. There is a 10% withholding at the time of making payments to investors, which the investors can claim credit for while filing their returns.

Reflections from my first syndicate in November 2020:

I had also never raised an syndicate deal before – so in parallel with these discussions, @LandonAinge, the MD of @ASyndicates was walking me through the legal and financial regulations on the back office side of setting up an SPV.

Lesson 1. Some investors will ask LOTS of questions, some will ask very few. That’s normal, people have different levels of information they need to be able to have conviction in an investment.

Lesson 2. Keep a list of all the questions potential investors ask you & the answers you have for them in a central spot (I used Notion) to make things more efficient.

Lesson 3. Use a CRM. I didn’t – and a combination of twitter DMs and separate email threads got messy fast. I’ll be using Notion going forward to keep tabs on investors in my network & their thesis areas.

Lesson 4. Celebrate quick nos & long yes. I loved when angels were able to say a quick no based on their thesis, and on the flip side it was incredible to hear a yes after playing email tag for a week & answering deep dilligencing questions.

Lesson 5. The doldrums happen when you’re so close you can taste it. About one or two investments from finishing, i was waiting on a handful of stalled conversations. Have patience, they’ll come through.

Lesson 6. Follow up. Follow up. Follow up. This is incredible important to closing a syndicate quickly and making sure you’re communicating the necessary information.

Lesson 7. Nerves mean you’re doing something right. I needed to lay down and take some very deep breaths the morning after asking for allocation. Executing on small tasks over and over make things seem less scary.

Lesson 8. I was considering this from the beginning, but trying to focus on angels with similar or tangential interest area cut my reach outs in half vs had I not been specific. The more closely a company aligns with their thesis, the easier it is to reach conviction.

Lesson 9. There is no better way to learn than to do, and do repeatedly. The perspective I gained talking to angels helps me anticipate what they may ask in the future which contributes to the advice I can provide founders & my general knowledge of investing.

Lesson 10. The only thing that feels better than doing my own syndicate, is doing it with an INCREDIBLE team backing me…

More resources: